Death of Taylor rule principle

Death of Taylor rule principle

The main casualty of recent inflationary spike was the Taylor rule for monetary policy, and especially the Taylor rule principle.

With the global inflationary spike coming to an end, it is time to re-consider our macroeconomic models and see how they did.[1] There was a lot of talk (and criticism) focused on the Phillips curve model, based on which many claimed we will need high unemployment rate to bring down inflation. It is clear that the simple Phillips curve perspective has proven to be wrong, even though as Mike Konczal points out in his piece, modern Phillips curve models allow for lower inflation without higher unemployment rate.

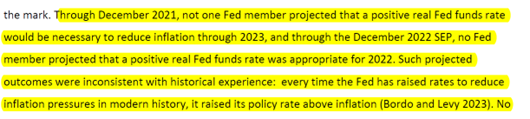

In other words Phillips curve does not have to be dead. But instead of Phillips curve I think there is one concept that does deserve to be dead, at least if taken literally as prescription for monetary policy: The famous Taylor rule and the Taylor rule principle, which states that to contain inflation policy rates have to increase more than inflation.[2] The idea is of course simple: we need positive real interest rates to bring inflation lower, something that was the case historically. Indeed, some people were outright mocking the central banks about their forecasts that include inflation genie getting back into the bottle without real rates becoming positive. Here is an example from paper from spring of this year (!):

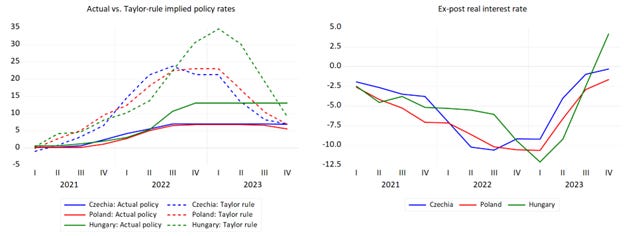

Of course, we now know that we did not need positive real rates to defeat inflation. As I was writing earlier this year, the policy rates in US never went to, much less above the levels suggested by the Taylor rule.[3] But this is not only US: euro zone has defeated a double digit inflation with interest rates in low single digits. And most striking is the example of CEE countries, where inflation went to almost 20% and inflation expectations should be less anchored than in advance economies. And yet it looks like that inflation was defeated with interest way below inflation:[4]

From all this examples it is clear that the Taylor rule and the principle were a terrible guides for monetary policy in current inflationary spike. Why is that so given that in worked so well in history? As with many things that work in history but then suddenly don’t, the problem is that the current situation is different from the historical experience (yes, this time is sometimes different). Historically increases in inflation were either result of overheated demand or of supply shocks that translated into higher structural inflation (through inflation expectations, if you want).[5] But this time around a lot of the inflation was about temporary supply shocks, which reversed in due course, bringing inflation down.

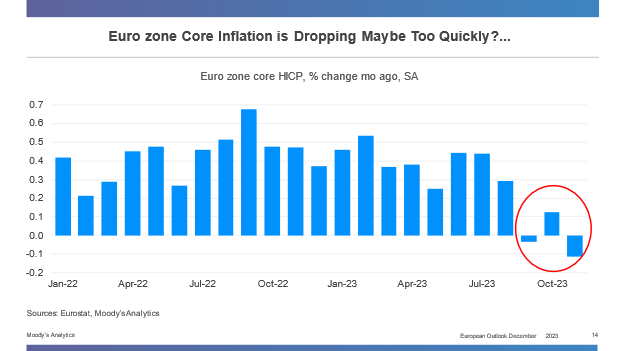

Indeed the failure of Taylor rule prescriptions is in my mind the best argument that the inflationary spike was after all transitory, just that it was very long-transitory: If inflation came down with disproportionally small reaction by central banks then it must have been coming down on its own.[6] This is becoming clearer and clearer over time, especially in euro zone. In 2022 I had piece arguing that for inflation to be truly transitory we will need to see inflation below the target – otherwise people will be able to argue that inflation decreased because of central bank target and that without such action it would remain elevated. Well, guess what? In euro zone we seem to be on our way to below-target inflation, given that the latest numbers are showing core inflation momentum at 0%, or maybe slightly negative:

While this is overstating the case how soft the core will be in future months, it is entirely possible that inflation will come significantly at sub-2% values next year and in 2025. Especially given that food price disinflation has still not arrived in full. We will have to wait for another year or so to see how get confirmation whether inflation in eurozone was transitory and ECB has overreacted. But already now it is clear that Taylor rule and its principle have taken a huge blow. And while I don’t think it should be consigned to graveyard – it still has its added value - I do think that using it as a guide for monetary policy in all circumstances should be laughed at.

[1] Noah Smith had a good big picture piece on different schools of thought.

[2] I am being bit imprecise here – the principle is important as part of the rule, not necessarily for every single episode. Bus, as I show below, people were applying the Taylor rule as a prescription for current episode as well, so they were taking it literally as prescription for monetary policy.

[3] This is even true if one uses core inflation rather than headline inflation as the measure of inflation in Taylor rule.

[4] While the picture looks bit less extreme if one uses core inflation, it does not change much: In all the countries core inflation also reached double digit values.

[5] Here the past adherence to Taylor rule by central banks likely played a key role, as it created credibility that inflation will be brought back to the target, anchoring the expectations in current episode.

[6] Also note that the skepticism about we won’t need positive real interest rates and that inflation is transitory inflation was often connected. For example the above cited paper criticizes them both in single sentence:

Thank you for this piece; as always, it is very informative. I agree that the inflation was probably long-transitory, but this still begs the question: why didn't (historically still significant) interest rate increases hammer the economy into recession? However, if the disinflation was long-transitory it might just prove that the monetary lags would be such as well.

Pushing on the interest rate string in itself never did anything much, it was always about regime enforcement. Clever People can always make any "rule" fit the circumstances.