The future of eurozone consumer food prices

The future of eurozone consumer food prices

Food inflation is destined to collapse and might even go negative on sustained basis.

In previous two posts I have discussed that consumer food prices are elevated relative to agriculture prices, even if less than some might believe, and that it was the speed of the pass-through what is most shocking about recent consumer food inflation. Where does this leave us in terms of outlook for consumer food prices? Here I will show and discuss forecast from several models under two sets of assumptions for agriculture prices, and then consider how does a reasonable forecast look.

Agriculture prices assumptions

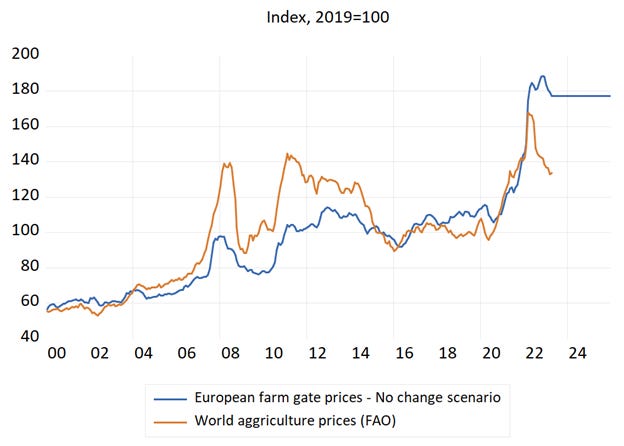

To forecast consumer food prices we need to first determine what is the future trajectory of agriculture prices. In absence of any specific knowledge there are two baseline scenarios I find plausible. One is assuming that European agriculture prices remain unchanged at their current values:

This amounts to a very conservative assumptions for several reasons. First, European agriculture prices are at historical extreme levels. It is easy to understand why they reached these extreme levels, given the invasion of Ukraine which lead to spike in energy and fertilizer prices as well as collapse in supply of agriculture products. It is harder to understand why they should stay at such levels despite most of the shocks (partly or fully) reversing. Second, the expectation for a decline is strongly supported by historical record, as jumps in agriculture prices have been always reversed later on. Lastly, we already know that world agriculture prices have declined substantially since their peaks, and it is hard to argue that European agriculture prices should not follow them eventually.

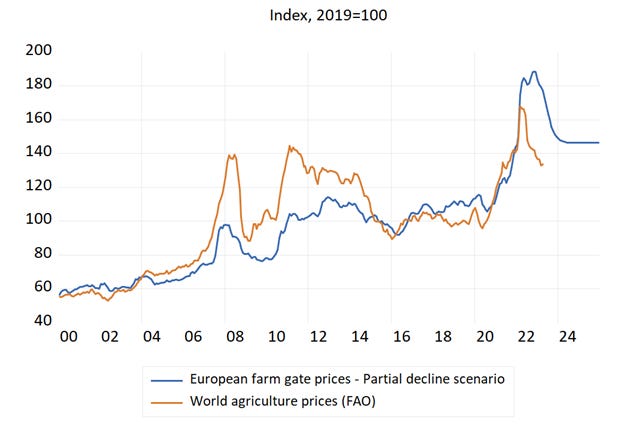

All this suggests that agriculture prices should decline, but it is hard to know how much. I will rely on simply heuristic and assume that agriculture prices will decline to half-way between their pre-pandemic level and post-pandemic peak.[1]

Note that this is still somewhat conservative assumption, as previous historical periods would suggest that we will return back at least close to pre-shock levels. We also know that world agriculture prices have already declined as much, so the assumption is equivalent to assuming that European agriculture prices catch up with world prices and that world prices do not decline further despite historical experience.

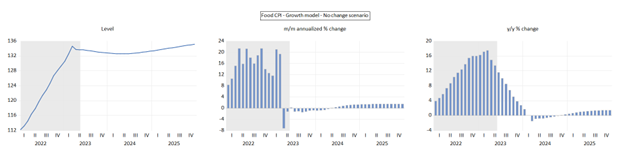

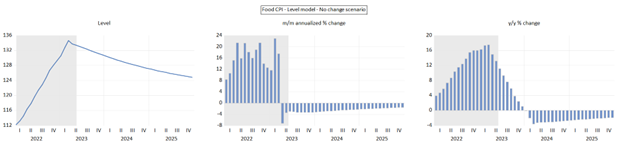

Forecasts with stable agriculture prices

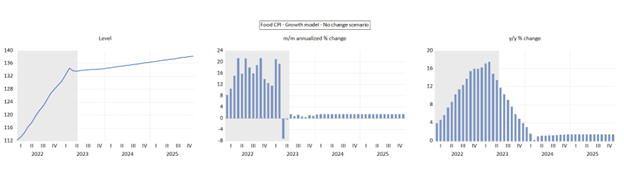

What happens when we take our growth and level models and feed them the flat agriculture prices path? The growth models will predict that consumer food prices will initially grow at a relatively slow pace, reflecting the recent downward dynamics in both consumer food prices and agriculture prices, before converging to historically average growth rate. This then translates into rapidly declining year-ago inflation rate for food, hitting zero in beginning of next year.

This is at a first look surprising. Didn’t the growth model suggest that consumer food prices are greatly inflated? Well, yes, they did. But no, this does not imply that the model will predict decline in food prices. Since the model is in growth rates, it does not care about the level of food prices. All it takes into account is recent dynamics in consumer food prices, together with recent and future dynamics in agriculture prices. If agriculture prices remain unchanged, as we assume here, then consumer food prices will mostly remained unchanged, irrespective of the relative levels of the two.

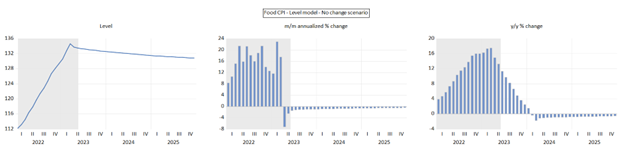

This contrasts with the model specified in levels. Since this model suggests that consumer food prices are too high relative to agriculture prices, and since the model reflects this kind of information in its forecast, then the forecast is that food inflation will be subdued in coming years. That said, since the model includes very strong propagation, the convergence to the “correct” level of food prices will be only very gradual. As such, the model predicts only very small declines in food prices, which are though lasting for long time . The year-ago inflation rate declines faster, but not much faster, than in case of the growth model forecast, and stays mildly negative until the end of our forecast horizon.

One word of caution is in order: we saw in earlier that there is a reason to believe that the level models are overstating the degree to which food prices are currently too high; since the forecast presented here does not correct for that, it might be overstating the length/magnitude of the price declines.

Forecasts with dropping agriculture prices

What changes if we assume more realistic path for agriculture prices? Unsurprisingly, this will imply lower consumer food price inflation. In case of the growth rate model this translates into relatively moderate but protracted period of declines in food prices. This reflects the gradual pass-through from lower agriculture prices into lower food prices. Overall food prices are predicted to decline by 1% over the period of one year, with the minimum year-ago inflation rate of around -1% reached next spring.

Meanwhile, for the level model the effect of lower agriculture prices is more meaningful. This reflects two aspects. First, the pass-through from agriculture prices to food prices is estimated to be stronger. Second, even in absence of decline the model was predicting negative growth in food prices. Overall, food prices are predicted to decline by 8% by the end of 2025, and to continue declining afterwards. The year-ago inflation rate hovers around 3% throughout this time.

Taking stock

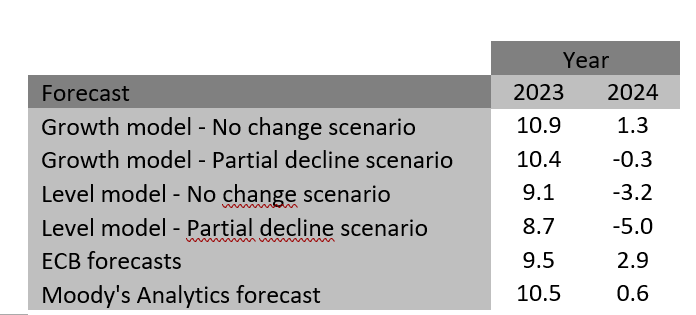

So where does this leave us overall? Table below provides summary of the forecasts in terms of annual averages. It also includes ECB’s forecast and Moody’s Analytics forecast for comparison:

While different assumptions and different models imply very different outlooks, there is some general lessons we can take. First, no matter the assumptions or model, year-ago food inflation should decline pretty rapidly during this year.[2] Indeed, even the most “aggressive” forecast, corresponding to using growth model and assuming no decline in agriculture prices, features year-ago inflation rate touching 0 in spring of next year. Therefore, in absence of new shocks pushing agriculture prices higher, it is hard to see how food price inflation does not collapse in remainder of this year, and does not stay subdued for a period of time. In light of this it is hard to see how do we get to ECB’s 2024 forecast number, as I pointed out back when forecasts were published.

Second, if we assume that farm gate prices continue declining then both models suggest that year-ago inflation rate will go negative on sustained basis. The difference is only how much and for how long. Is an outright decline in consumer food prices a reasonable forecast? On one hand, sustained decline in food prices is something we have never observed; at most there were periods of a prolonged stagnation, like in 2009 and 2014.

On the other hand, price developments over last few years have been unprecedented. Who is to say that the unprecedented on the way up will not be followed by the unprecedented on the way down? Simply, excessively high food prices and dropping agriculture prices is something we have never seen before and it might just be the powerful combination that translates into outright food price declines.

Still, with recent developments being so unusual, a dosage of skepticism in own conclusions is surely warranted. For example, the estimated models do not include other input costs such as energy and more importantly wages, which will continue to grow quickly. This is why I am hesitant to go all out with the forecast of large declines in food prices, which one would do if he was willing to bet everything on what the models say. At the same time, the models are clearly telling us something. So overall I feel like penciling in a prolonged period of no growth in food prices is the best proposition.

[1] Specifically, I use an error-correction speciation with the equilibrium level determined as described in the text, error-correction coefficient of 0.1, implying 10% of the dis-equilibrium is eliminated each months, and a lagged dependent variable to ensure smoothness. With lower error-correction coefficient the decline

[2] Of course, one can imagine scenarios where this is not true – it would just take another large agriculture price shock. But (a) given the starting level, that is not so straightforward to imagine, (b) it is for sure not part of neutral baseline outlook.