The off-the-charts pass-through in consumer food prices

The off-the-charts pass-through in consumer food prices

It was the speed of pass-through that made eurozone food inflation so crazy and different from previous historical periods, not the size of the increase per-se.

In the previous post I argued that, while eurozone consumer food prices seem to be too high given the price of agriculture prices, they are not as high as one might think based on simple analysis. But this is not the end of the story. After all, the rise in food prices over last 1,5 years was simple unprecedented:

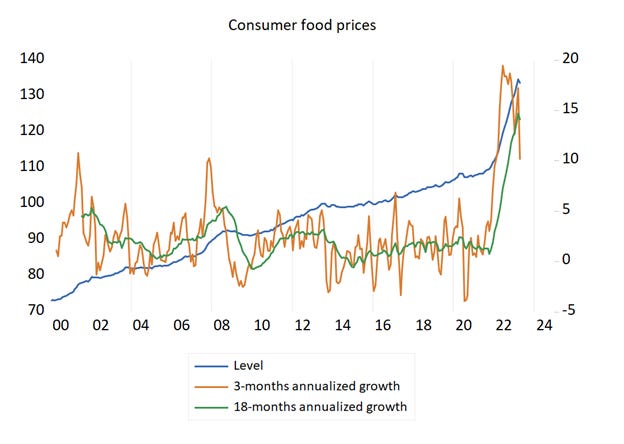

This can be seen directly from the long-term chart of level of food prices (blue line), but looking at longer-period growth rate highlights this face even mode: the increase over last 18 months is triple of the previous historical maximum (green line).

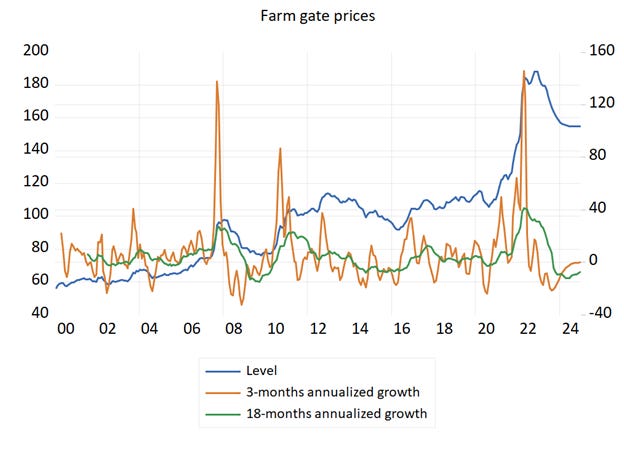

What is behind this? Of course, large part of the story is the increase in agriculture prices. But importantly, this cannot be the whole story, as the increase in agriculture prices was nowhere as unusual in historical perspective as what we saw in consumer food prices: Either at 3-month annualized or 18-months annualized growth rate the increase was on par with previous historical maxima.

So what made our current experience so unique is not just the size of increase in agriculture prices, which meant that consumer food prices had to increase by a lot. It was also the speed by which the higher agriculture prices were translated into higher consumer food prices. And in some sense, it was this speedy pass-through which stands out as really unusual, not the size of the increase.

Revisiting model in levels

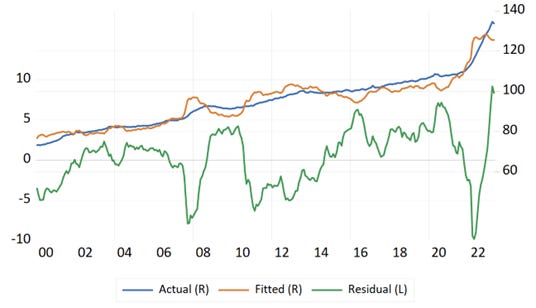

This was visible already in the previous post. For example, looking at the fit of the model in levels during the most comparable historical period, 2007-2008, the different behavior of consumer food prices is especially visible. Back then, agriculture prices have skyrocketed to a similar, if slightly smaller degree as last year. But consumer food prices followed only very hesitantly. Indeed, based on the model, consumer food prices were too low throughout 2007 and most of 2008, as consumer food prices increases lagged behind agriculture increases. They became too high only when agriculture prices dropped at the end of 2008.

This is in contrast to current experience, where consumer food prices became too high before agriculture prices declined measurably. This is then the key distinguishing feature of current episode: unlike during previous historical periods of high agriculture prices, this time around consumer food prices caught up with high agriculture prices, and they did so very rapidly.

Looking at dynamic model

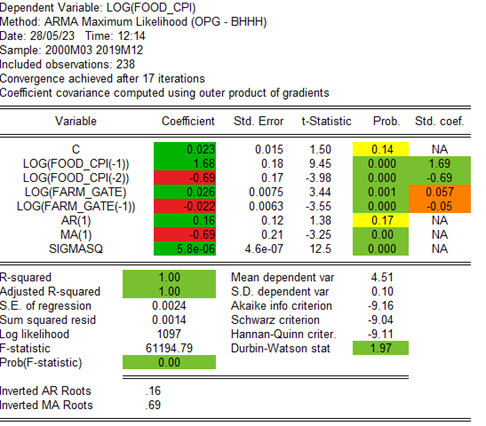

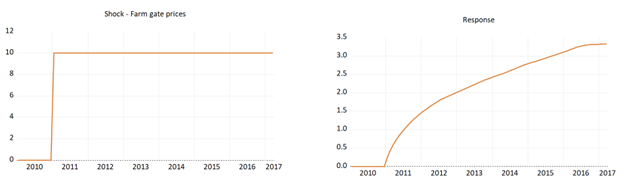

Another way to investigate how unusual was the speed of the pass-through, is to take our level model and make it into an actual useful model for forecasting. The initial model is an equilibrium model in the sense that predicts what the consumer food prices should be in the long-run equilibrium given the agriculture prices. Of course, this makes it a poor model for forecasting movements in consumer food prices, as there is always a gradual adjustment to the equilibrium. To make is a useful model for forecasting we would need to include additional dynamic terms and make it ARDL-type model. A proper final model would look something like this:

The key aspect of the model is that the pass-through from the agriculture prices to consumer food prices is gradual. Indeed, it is very gradual, with only half of the response occurring within a year, and something like 5 years before the full response:

Applying this model to our current experience highlights how it was the speed, not the magnitude of the increase, that really stands out. We already saw that the level model suggests that the magnitude of the increase was usual only by a moderate amount.[1] But irrespective of this the consumer food prices are significantly higher than what the dynamic level model would expect them to be at this point in time:

The reason of course is that based on the historical patterns of behavior food prices should have been reflecting high agriculture prices at much slower pace than they did. By this spring they should have increased only by 8% from their summer-2021 level, and then another 4% in rest of this year (and more in later years).

Takeaways

The takeaway is that it was not the size of the increase in consumer food prices, which was highly unusual, even if it was to some degree. Rather, it was the speed of the increase which was simply shocking. And this is not just an issue of timing, in the sense that we would have gotten the increase sooner or later anyway. This is because European agriculture prices seem to be already declining and are likely to continue. It is very likely that if consumer food prices would be as slow as usual to increase, then their overall increase would be actually significantly smaller. Simply, they would have missed the peak in agriculture prices, much like they did during 2007-2008 period.

Why did consumer food prices catch up with agriculture prices faster than during previous historical periods? That is a hard question to answer, with several plausible answers. But personally I think it was the fact that we got a multiple supply shocks at the same time. The key thing to realize that price setting is a coordination game. In situation when all producers are hit with multiple cost-push shocks - not just food, but also energy, wages and materials – they know that everybody will be forced to increase prices. In such situation the usual hesitancy to increase prices due to worries about market share goes out of the window, and we get coordinated rapid price increases.

[1] The dynamic level model suggests somewhat smaller pass-through than the static level model, but not to a degree that would change our conclusions.